Funeral Fallout: MIL Furious Over Widow’s Unexpected Inheritance

After the sudden death of her husband in his 40s, a grieving widow finds herself entangled in a bitter feud with her mother-in-law over life insurance money. In the early days of her grief, the widow gratefully accepted her mother-in-law’s offer to cover funeral costs—a gesture made during a haze of sorrow and shock. Months later, she remembered a life insurance policy she had through her job, naming her late husband as the insured, and sought the payout to rebuild her life.

When the mother-in-law discovered the existence of the policy and the payout, everything turned hostile. She demanded reimbursement for the funeral expenses and accused the widow of being selfish for keeping the money. The accusations struck hard, painting the widow as opportunistic rather than grieving—adding a layer of emotional chaos to an already unbearable loss.

To the widow, however, the insurance money represents more than finances—it’s the last link to a life that was abruptly shattered. She hopes to use it to move closer to her own family and begin healing. Though she understands her mother-in-law’s pain, she’s blindsided by the venom and wonders if choosing her own survival makes her the villain in someone else’s story.

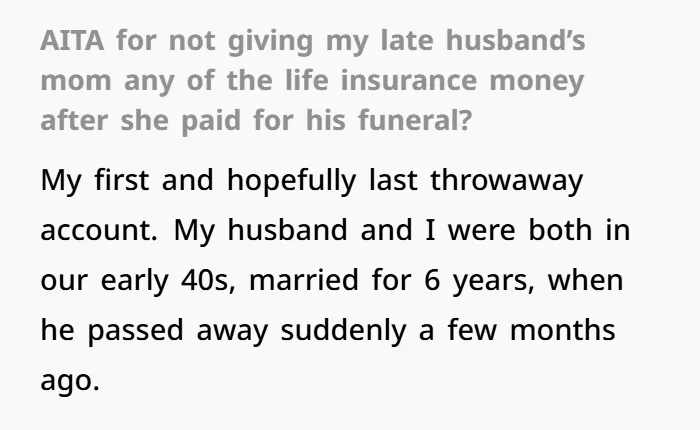

The author of the post recently lost her husband, with whom she had shared six years of marriage.

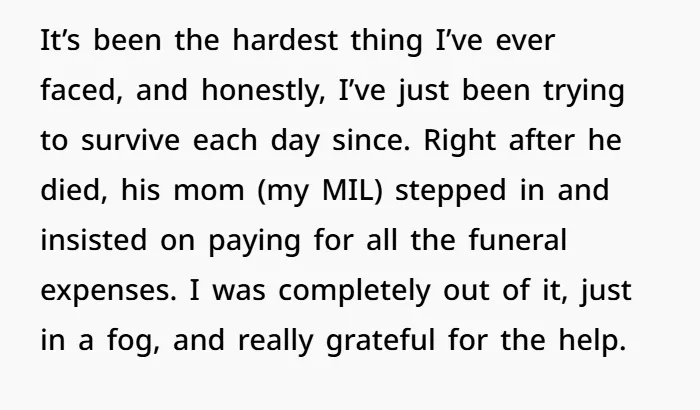

It was a devastating loss for the woman, and she felt deeply grateful to her mother-in-law for stepping in to cover all the funeral costs.

The Stark Economics of Saying Goodbye

Across the globe, funerals are an emotionally taxing affair made heavier by their steep price tags. In the United States, an average funeral can drain between $7,000 and $12,000, according to the National Funeral Directors Association. The mother-in-law’s decision to foot the bill may appear both selfless and strategic—an attempt to swiftly manage a pressing expense in a moment of chaos. However, when financial boundaries aren’t discussed beforehand, these gestures often morph into battlegrounds of misaligned expectations. In this case, the widow hadn’t yet learned about her late husband’s life insurance policy. Unprepared and grieving, she couldn’t have foreseen the firestorm that followed.

Who Gets What: The Legal Fine Print

Legally, a life insurance payout belongs solely to the individual named as the beneficiary. It is not a shared inheritance, nor an open fund for collective mourning. Its intent is to help the surviving beneficiary manage immediate and long-term needs—be it mortgage payments, debt clearance, or simply staying afloat. Unless a prior agreement was made to repay the funeral costs, there’s no lawful obligation for the widow to do so. As Investopedia clearly outlines, without a signed contract or verbal commitment, beneficiaries have the right to prioritize their financial future without guilt.

The Heartache Beneath the Headlines

While the widow acted within her rights, she now finds herself at the crossroads of moral and emotional responsibility. Her mother-in-law’s simmering resentment likely stems from unprocessed grief an overwhelming blend of heartbreak, helplessness, and a sense of being sidelined. Grief often distorts fairness and fuels entitlement, especially when money becomes a substitute for emotional control. Meanwhile, the widow is left to reconstruct a life that’s been torn apart finding housing, facing solitude, and redefining her stability. Though she owes nothing legally, a small gesture perhaps reimbursing a portion of the funeral cost could serve as both a peace offering and an emotional salve in a storm still raging on both sides.

- Transparent Dialogue: A sincere and composed conversation between the widow and her mother-in-law could serve as the first step toward healing. By openly sharing how the insurance payout is essential for securing her future covering housing, living costs, or even therapy the widow can humanize her choices and potentially shift the emotional tone.

- Meeting Halfway: Though she holds no legal responsibility to repay the funeral expenses, extending a partial contribution as a gesture of goodwill might ease tensions. This small act of empathy could go a long way in rebuilding trust and showing respect for her mother-in-law’s support during a painful time.

- Professional Mediation: When emotions cloud communication, turning to a neutral third party like a family therapist or mediator can create a safe space for both voices to be heard. A guided dialogue may help untangle misunderstandings and guide the family toward a solution that respects both grief and financial boundaries.

Case Studies of Comparable Disputes

Clashes over life insurance proceeds and estate division are far from rare. In fact, a study published in the Journal of Financial Therapy revealed that vague communication and unspoken assumptions frequently ignite posthumous family discord surrounding financial legacies. When expectations remain undefined, even grief can turn combative. Clear-cut arrangements especially those documented in writing—serve as powerful deterrents against such turmoil. These findings underscore a critical truth: no matter how emotionally charged the moment, it remains imperative for family members and former spouses to delineate financial responsibilities before the storm breaks.